Latest ads

-

Power Lifting Lever Belt

Power Lifting Lever Belt- SkullVamp

- Updated:

-

port.lk Domain for sale

- Lankan-Tech

- Updated:

-

Colombo Kaduwela - Two Storey House for Sale

Colombo Kaduwela - Two Storey House for Sale- dilrasan

- Updated:

-

Wechat qr verification

- Pawan2005

- Updated:

-

🚀 GOOGLE AI PRO 18 MONTHS ACTIVATION 🚀

🚀 GOOGLE AI PRO 18 MONTHS ACTIVATION 🚀- sayuru bandara

- Updated:

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

")

year 10 sylabus 1 da thibbe?xcorect said:Kauda danne wal poli hadana suthraya

කවුද දන්නේ වැල් පොලී හදන සූතය

OL walata thibbaAirtel said:year 10 sylabus 1 da thibbe?

mata eka danaganna ona ban

dan e poth koheda danneth na

umba dannawada

mathaka ne banxcorect said:OL walata thibba

mata eka danaganna ona ban

dan e poth koheda danneth na

umba dannawada

man laga thiyena teachers guide 1 withrai

eke ne

http://www.nie.sch.lk/ebook/s11tim15.pdf

")

Mathematics of interest rates

[edit] Simplified Calculation

Formulae are presented in greater detail at time value of money.

In the formulae below, i or r are the interest rate, expressed as a true percentage (i.e. 10% = 10/100 = 0.10). FV and PV represent the future and present value of a sum. n represents the number of periods.

These are the most basic formulae:

The above calculates the future value of FV of an investment's present value of PV accruing at a fixed interest rate of i for n periods.

The above calculates the future value of FV of an investment's present value of PV accruing at a fixed interest rate of i for n periods.

The above calculates what present value of PV would be needed to produce a certain future value of FV if interest of i accrues for n periods.

The above calculates what present value of PV would be needed to produce a certain future value of FV if interest of i accrues for n periods.

or

or

The above two formulae are the same and calculate the compound interest rate achieved if an initial investment of PV returns a value of FV after n accrual periods.

The above two formulae are the same and calculate the compound interest rate achieved if an initial investment of PV returns a value of FV after n accrual periods.

The above formula calculates the number of periods required to get FV given the PV and the interest rate i. The log function can be in any base, e.g. natural log (ln)

The above formula calculates the number of periods required to get FV given the PV and the interest rate i. The log function can be in any base, e.g. natural log (ln)

[edit] Compound

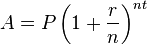

Formula for calculating compound interest:

Where,

A. Using the formula above, with P = 1500, r = 4.3/100 = 0.043, n = 4, and t = 6:

So, the balance after 6 years is approximately $1,938.84.

[edit] Translating different compounding periods

Each time unpaid interest is compounded and added to the principal, the resulting principal is grossed up to equal P(1+i%).

A) You are told the interest rate is 8% per year, compounded quarterly. What is the equivalent effective annual rate?

The 8% is a nominal rate. It implies an effective quarterly interest rate of 8%/4 = 2%. Start with $100. At the end of one year it will have accumulated to:

$100 (1+ .02) (1+ .02) (1+ .02) (1+ .02) = $108.24

We know that $100 invested at 8.24% will give you $108.24 at year end. So the equivalent rate is 8.24%. Using a financial calculator or a tableis simpler still. Using the Future Value of a currency function, input

$100 (1+ .009853) (1+ .009853) (1+ .009853) (1+ .009853) = $104

$100 (1+ .009853) (1+ .009853) (1+ .009853) (1+ .009853) = $104

The mathematics to find the 0.9853% is discussed at Time value of money, but using a financial calculator or table is easier. Input

$100,000 (1+ .1247) (1+ .1247) (1+ .1247) (1+ .1247) = $160,000

Find the 12.47% annual rate the same way as B.) above, using a financial calculator or table. Input

In January 1970 the S&P 500 index stood at 92.06 and in January 2006 the index stood at 1248.29. What has been the annual rate of return achieved? (ignoring dividends).

[edit] Answer:

[edit] Doubling

The number of time periods it takes for an investment to double in value is

where

where

is the interest rate as a fraction.

is the interest rate as a fraction.

Let p be the interest rate as a percentage ( i.e., 100 i ). Then the product of p and the doubling time t is fairly constant:

interest doubling time product

[edit] Periodic compounding

The amount function for compound interest is an exponential function in terms of time.

Since the principal A(0) is simply a coefficient, it is often dropped for simplicity, and the resulting accumulation function is used in interest theory instead. Accumulation functions for simple and compound interest are listed below:

Note: A(t) is the amount function and a(t) is the accumulation function.

Note: A(t) is the amount function and a(t) is the accumulation function.

[edit] Simplified Calculation

Formulae are presented in greater detail at time value of money.

In the formulae below, i or r are the interest rate, expressed as a true percentage (i.e. 10% = 10/100 = 0.10). FV and PV represent the future and present value of a sum. n represents the number of periods.

These are the most basic formulae:

[edit] Compound

Formula for calculating compound interest:

Where,

- P = principal amount (initial investment)

- r = annual nominal interest rate (as a decimal)

- n = number of times the interest is compounded per year

- t = number of years

- A = amount after time t

A. Using the formula above, with P = 1500, r = 4.3/100 = 0.043, n = 4, and t = 6:

So, the balance after 6 years is approximately $1,938.84.

[edit] Translating different compounding periods

Each time unpaid interest is compounded and added to the principal, the resulting principal is grossed up to equal P(1+i%).

A) You are told the interest rate is 8% per year, compounded quarterly. What is the equivalent effective annual rate?

The 8% is a nominal rate. It implies an effective quarterly interest rate of 8%/4 = 2%. Start with $100. At the end of one year it will have accumulated to:

$100 (1+ .02) (1+ .02) (1+ .02) (1+ .02) = $108.24

We know that $100 invested at 8.24% will give you $108.24 at year end. So the equivalent rate is 8.24%. Using a financial calculator or a tableis simpler still. Using the Future Value of a currency function, input

- PV = 100

- n = 4

- i = .02

- solve for FV = 108.24

The mathematics to find the 0.9853% is discussed at Time value of money, but using a financial calculator or table is easier. Input

- PV = 100

- n = 4

- FV = 104

- solve for interest = 0.9853%

$100,000 (1+ .1247) (1+ .1247) (1+ .1247) (1+ .1247) = $160,000

Find the 12.47% annual rate the same way as B.) above, using a financial calculator or table. Input

- PV = 100,000

- n = 4

- FV = 160,000

- solve for interest = 12.47%

In January 1970 the S&P 500 index stood at 92.06 and in January 2006 the index stood at 1248.29. What has been the annual rate of return achieved? (ignoring dividends).

[edit] Answer:

[edit] Doubling

The number of time periods it takes for an investment to double in value is

Let p be the interest rate as a percentage ( i.e., 100 i ). Then the product of p and the doubling time t is fairly constant:

interest doubling time product

[edit] Periodic compounding

The amount function for compound interest is an exponential function in terms of time.

- t = Total time in years

- n = Number of compounding periods per year (note that the total number of compounding periods is

)

- r = Nominal annual interest rate expressed as a decimal. e.g.: 6% = 0.06

Since the principal A(0) is simply a coefficient, it is often dropped for simplicity, and the resulting accumulation function is used in interest theory instead. Accumulation functions for simple and compound interest are listed below:

m doo said:Minissunta gini gedi denda neda set wenne?

Pissuda heenenwath ehema hithanne na

oyage sigiyanam cha wage

hena loku file ekakne

sigiya open wenna patta welawak yanawa

oka aththatama sigi yakda

xcorect said:Pissuda heenenwath ehema hithanne na

oyage sigiyanam cha wage

hena loku file ekakne

sigiya open wenna patta welawak yanawa

oka aththatama sigi yakda

Its ok dude.... but oyage ekanam maxxa... patta graphics... matath ekak hadala denda berida brother? lol

m doo said:Its ok dude.... but oyage ekanam maxxa... patta graphics... matath ekak hadala denda berida brother? lol

Mokakda mata molawan kiyanne

xcorect said:Mokakda mata molawan kiyanne

ok ok now i understood... use spectacles.... its mita molawagena... not mata molawagena.... that means atha mita molawanawa kiyanne...

Similar threads

- Replies

- 5

- Views

- 93

- Replies

- 0

- Views

- 197

- Replies

- 1

- Views

- 292